Assessing responsibilities is key to real estate investment decisions. Analyzing operational costs, comparing to industry standards, and leveraging data analytics tools aid informed choices. Balancing immediate needs with long-term goals through strategic budgeting and resource allocation optimizes savings while managing real estate responsibilities effectively. A multifaceted approach includes financial analysis, targeted investments, and regular adjustments to adapt to evolving circumstances and market trends.

In the dynamic landscape of real estate, balancing responsibilities with maximizing savings is a delicate dance for investors and property managers alike. As markets fluctuate and expectations rise, understanding how to weigh duties against financial gains becomes crucial for sustainable success. The challenge lies in recognizing that while cost-cutting measures are essential, neglecting day-to-day obligations can lead to long-term losses and diminished asset value. This article provides a comprehensive framework to navigate this intricate equilibrium, offering expert insights tailored to enhance efficiency and profit margins without compromising core responsibilities in the real estate sector.

Assess Responsibilities: Weighing Costs Across Properties

When navigating real estate investments, assessing responsibilities is a critical step in weighing costs across properties. Each property comes with its unique set of obligations, from maintenance and repairs to tax payments and insurance. For instance, older buildings may require substantial capital for renovations, while newer constructions might have higher utility expenses. Landlords or investors must meticulously examine these expenses to ensure financial sustainability. A comprehensive analysis involves breaking down operational costs into fixed and variable categories, allowing for a clear understanding of budget allocation.

Consider the case of a multi-family apartment complex. Responsibilities include property management fees, regular maintenance such as landscaping and building security, and major repairs like roof replacements or HVAC system overhauls. Comparatively, a commercial office space may have higher utility costs due to increased occupancy, but it might also benefit from lower property taxes if located in areas with tax abatements. Expert advice suggests benchmarking these expenses against industry standards to gauge competitive pricing and identify potential cost-saving opportunities.

Real estate investors can enhance their decision-making by utilizing data analytics tools that track historical property performance. These tools provide insights into how responsibilities impact overall savings, enabling more informed choices. For instance, a study by the National Association of Realtors (NAR) revealed that well-maintained properties with efficient energy systems consistently command higher rental rates and sell for premium prices. As such, investing in proactive maintenance and energy upgrades can be a strategic move, balancing short-term costs against long-term gains.

Calculate Savings: Real Estate's Impact on Your Budget

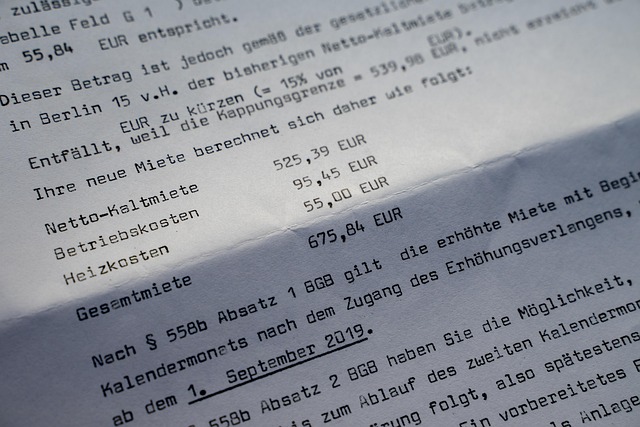

Calculating savings is a crucial step when weighing responsibilities against overall financial health. In the context of real estate, this evaluation becomes paramount as property ownership significantly impacts your budget. The initial cost of purchasing a home or investing in real estate can be substantial, but it’s just the beginning of a long-term commitment. For instance, according to recent studies, the average homeownership cost, including mortgage payments, property taxes, and insurance, amounts to approximately 28% of total household income. This percentage varies based on location and specific market conditions, yet it underscores the substantial financial responsibility associated with real estate ownership.

Real estate’s impact extends beyond initial costs. Maintenance expenses, which can range from minor repairs to major renovations, are ongoing obligations. On average, homeowners spend around 1-4% of their home’s value annually on maintenance and repairs, as suggested by industry reports. These costs can quickly accumulate, especially for older properties. Conversely, renting offers more immediate financial flexibility, as rent typically represents a smaller portion of income compared to mortgage payments and property expenses. However, long-term savings potential should be considered, as investments in real estate often appreciate over time, providing an opportunity for substantial future gains.

To maximize savings, prospective homeowners must carefully analyze their budget. Tracking expenses related to housing, utilities, and community services allows for a clear understanding of the financial commitment. For instance, a study by the National Low Income Housing Coalition found that 30% of low-income households spend more than 50% of their income on housing costs, illustrating the importance of thorough budgeting. Additionally, exploring government incentives or programs designed to assist first-time homebuyers can provide significant savings opportunities. Consulting with financial advisors or real estate professionals who specialize in cost-effective ownership strategies is also beneficial. By carefully considering these factors, individuals can make informed decisions that balance responsibilities and overall savings goals.

Strategize Allocation: Balancing Needs with Financial Goals

When weighing responsibilities against overall savings, one of the most critical considerations is strategizing the allocation of financial resources—balancing immediate needs with long-term financial goals. This delicate dance requires a nuanced approach, especially in areas like real estate, where decisions can significantly impact both current and future financial stability. For instance, investing in a primary residence might be a top priority for many, offering not just shelter but also potential equity growth over time. However, this choice could divert funds from other goals, such as saving for retirement or funding children’s education.

Experts recommend a multi-faceted strategy to tackle this challenge. Firstly, conduct a thorough analysis of your financial landscape, including income, expenses, and existing assets. Categorize needs into essential (e.g., housing, utilities) and discretionary (e.g., entertainment, travel). Simultaneously, identify short-term and long-term financial goals, assigning them priority levels. For instance, paying off high-interest debt in the near term might be a higher priority than saving for a down payment on a second property. Once these categories are defined, allocate resources accordingly, ensuring that core needs are met while gradually working towards broader objectives.

In the context of real estate, this might entail purchasing a home at a reasonable price point, minimizing debt, and building equity over time. Alternatively, if your financial situation allows, investing in rental properties can provide passive income and long-term wealth generation. However, it’s crucial to consider the associated costs—maintenance, property taxes, insurance—and ensure these are factored into your savings strategy. A balanced approach could involve a combination of primary residence ownership and strategic investments, tailored to your unique financial profile and aspirations. Regularly reviewing and adjusting your allocation strategy is equally vital to adapt to changing circumstances and market conditions.